Euribor could drop to 2.5% next year as Spain drives economic growth in bloc

INTEREST rates in the Eurozone could fall to 2.5% next year, having closed August 2024 on 3.75%, according to latest research.

Sign in/Register

Looking for the Professionals/Advertiser Login?

By Signing up you are agreeing with our Terms and Privacy Policy.Forgot your password?

Feedback is welcome

MORTGAGES signed up in January this year have risen sharply based upon the same month in 2021 – although they still fall slightly short of levels seen prior to the pandemic.

According to the National Statistics Institute (INE), figures for the most recent complete calendar month available are for January 2022 as March has not yet concluded and February's numbers are still being crunched.

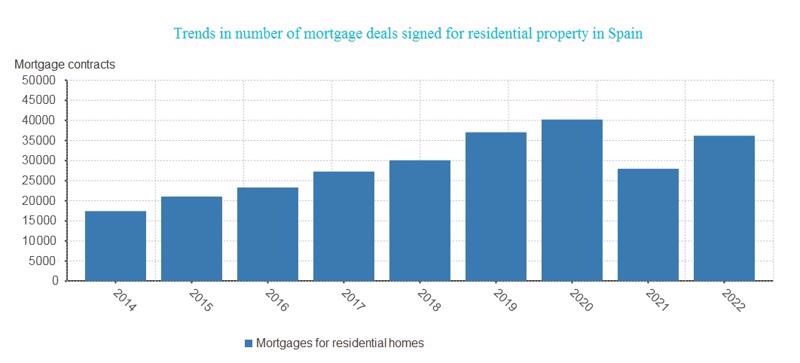

And for January, a total of 36,185 mortgage contracts for home purchases – as opposed to remortgages for renovations, or secured loans to buy commercial premises – were closed, being just under 90% of the total for the same month in 2020 when the word 'Coronavirus' was unknown outside medical research centres and the term 'Covid' not yet invented.

Even though the more than 40,000 mortgage deals sealed in the first month of 2020 has not been reached since, next year could be a different story, given that the year-on-year increase just reported is nearly 30%, or six times the annual rise registered for December.

Between December 2021 and January 2022, the number of new mortgages signed rose from month to month by 10%, and the amount of capital loaned by just under 7%.

As a result, the number of new mortgages taken out has been steadily rising for 11 consecutive months, much to the relief of the residential property industry which took a battering during the pandemic, particularly with the 2020 lockdown preventing any viewings or in-person visits to estate agency premises.

Capital rising

The INE reveals that the average sums borrowed for homebuying have gone up by 9.5% year on year, with a typical loan being for €141,427.

Overall capital lent to buyers in January 2022 totalled just under €5.12 billion – the highest figure for that month in 11 years and an annual increase of 41.7%.

Mortgages sold in the first month of a year have been continually rising since 2014, with around 17,000, to 2020, with just over 40,000 – the sharpest hike seen between 2018 (30,000) and 2019 (around 36,000) – taking a drop in January 2021 when Covid contagion rates were dramatically worse than they had been all year and when local areas and entire towns were being closed to non-residents with an evening curfew in place.

Back then, the number of mortgages granted was in region of 27,000 – slightly lower than in January 2017, albeit comfortably above the 23,000 or so in January 2016.

The most on the coasts (mainly)

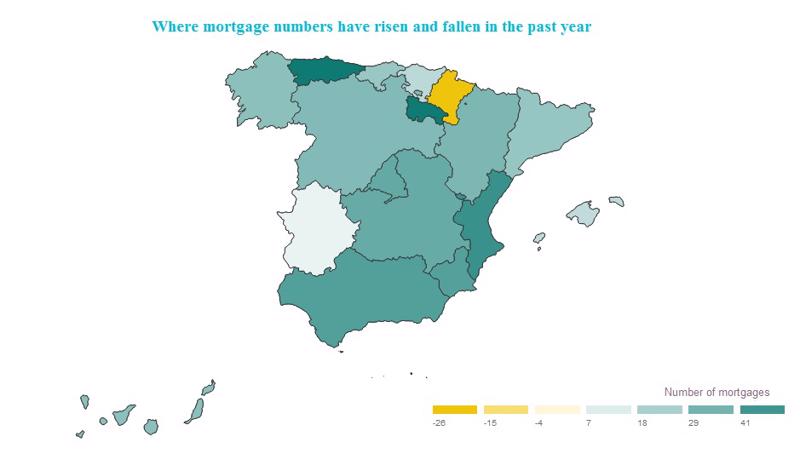

Andalucía, the region that makes up the southern strip of mainland Spain, saw the highest number of new mortgages signed for in January 2022 – a total of 7,644 – followed by the Greater Madrid region (6,063), Catalunya in the far north-east (5,833), and the Comunidad Valenciana, which occupies the middle stretch of the east coast (4,050).

The highest amount of total capital loaned was in Madrid, at just under €1.27bn, followed by Andalucía at nearly €977 million, and Catalunya at slightly below €954m.

Although these regions saw the largest numbers of new mortgages and highest sums lent, actual growth in percentage terms was greater in the north – in Asturias, on the north-west coast, home loan contracts shot up year on year by 51.7%, with the land-locked far-northern region of La Rioja only slightly behind, at 51.3%.

Very significant increases were seen in more heavily-populated coastal regions, too, however: The Comunidad Valenciana registered a 42.6% rise in the number of mortgages closed in January 2022 compared with January 2021, whilst Andalucía reported a hike of 37% and Murcia, 36.6%.

Only the far-northern inland region of Navarra – the capital of which is Pamplona – experienced an annual drop in mortgages signed, and a fairly drastic one, at 26.7%.

The Canary Islands registered a 24.7% increase, and the Balearics, 13.6%.

Fixed vs variable rates: Pattern turns upside-down overnight

Fixed-rate mortgages are rapidly gaining ground – having been very much in a minority since 2009, they suddenly shot upwards from around 5-10% to just over 40% of the total in around 2016, and now account for seven in 10 new home loans.

After its spike in 2007 and 2008, the Euribor, or Eurozone interest rate – upon which Spanish mortgages are based – gradually went into freefall and hit negative figures in February 2016 for the first time, where it has remained.

Analysts warned for years that the 'loan honeymoon' would not last forever, but although some rises have been seen periodically, the rate has remained well below zero and lower than when it first dipped into negatives.

But growing concern that price-led inflation might cause the European Central Bank (BCE) to raise rates to slow money circulation has led to more and more homebuyers seeking to freeze their interest for a set number of years.

Generally, along with a fee for fixing the rate, this type of mortgage tends to carry higher interest – as at January this year, on average, a fixed-rate loan is around 2.69%, whilst a variable-rate loan was typically about 2.21%.

The overall average interest rate for a home loan in January was 2.54%, one-tenth of a percentage point higher than the 2.44% of January 2021, and was typically for a repayment term of 24 years.

Mortgages in Spain are normally reviewed annually or, at most, six-monthly, meaning a variable rate does not mean sudden, unexpected hikes from month to month making it difficult to budget; instead, property owners can keep watch over the Euribor over time and, if they notice it starting to climb, have up to a year to plan whether or not to fix their rate ahead of its revaluation.

INTEREST rates in the Eurozone could fall to 2.5% next year, having closed August 2024 on 3.75%, according to latest research.

GRANTS of up to €250 are available this year for replacing older air-conditioning units in a bid to encourage greater energy efficiency.

MORTGAGE-LENDING has reduced dramatically in Spain in the past year, but that has not stopped homes on sale being snapped up: Over a third were purchased in cash, according to the latest figures.

RESIDENTIAL property sales have been shrinking consistently throughout 2023, but latest figures show this trend is relenting.